Construction demand for mineral products increased in the final quarter of 2020 everywhere outside of London.

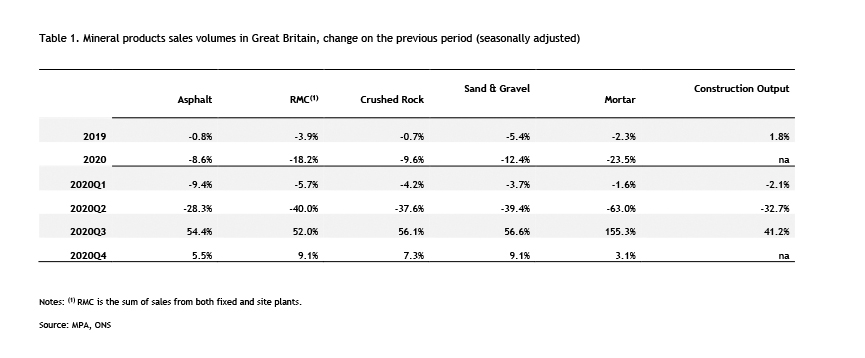

Recovery in the market for mineral products such as aggregates, concrete, asphalt and mortar was sustained during the fourth quarter of 2020, although full-year sales were down on 2019.

The analysis comes from the latest survey of the Mineral Products Association (MPA), which says the figures are encouraging although it also urges the Government to push on with delivering the UK’s planned infrastructure programme to support the economic recovery, construction and the supply chain.

The latest figures show that the faster than expected pickup in demand following the lockdown last spring continued. Sales volumes of ready-mixed concrete increased by a 9.1% in the fourth quarter (Q4) of 2020 compared with Q3, 7.8% for primary aggregates (crushed rock and sand & gravel), 5.5% for asphalt and 3.1% for mortar. Increases were recorded in most regions and the devolved nations in Great Britain, except in London, where volumes of ready-mixed concrete and asphalt saw renewed declines.

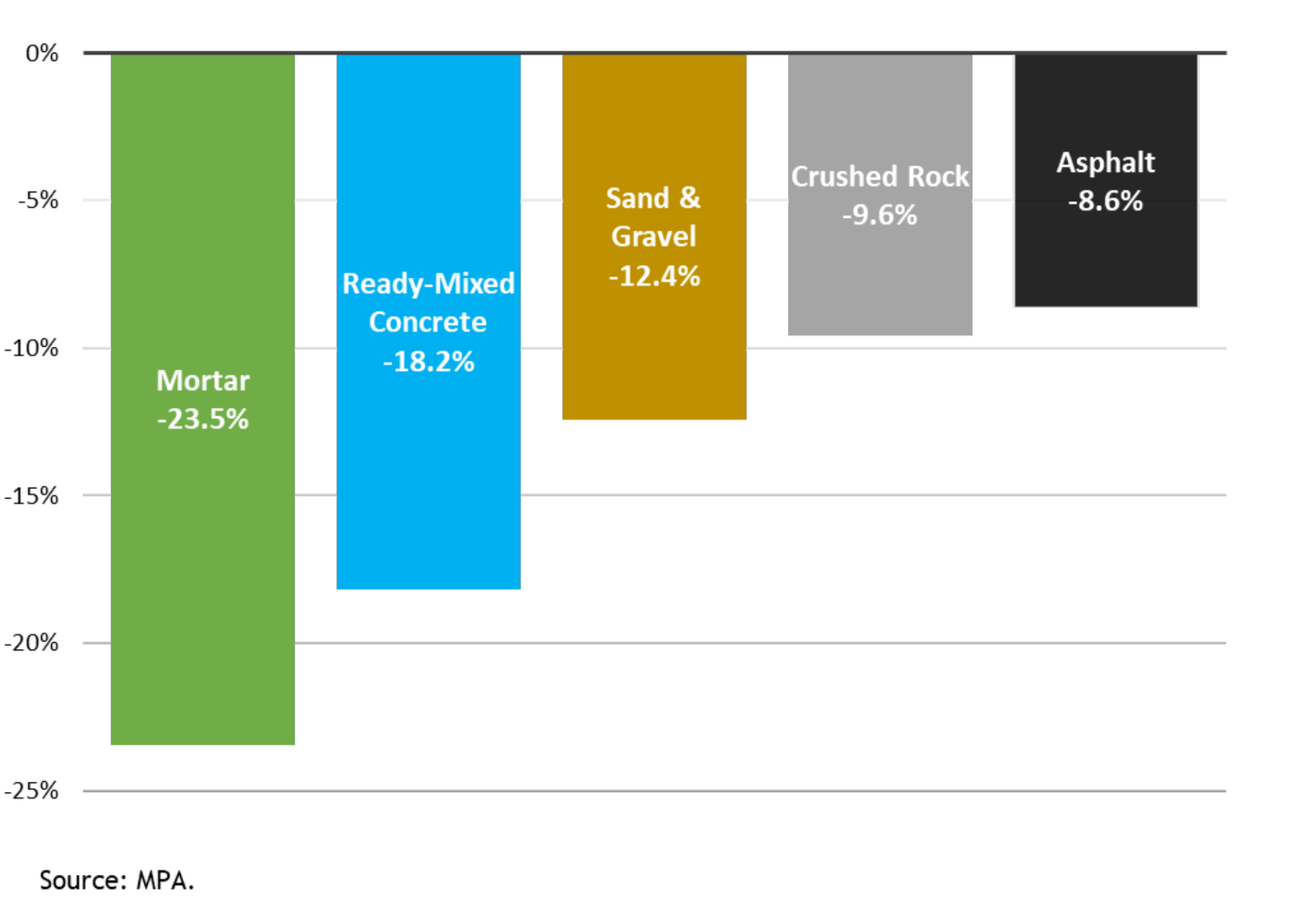

For the year and the UK as a whole, sales volumes in 2020 were still significantly down on 2019, with ready-mixed concrete and mortar sales the weakest, down 18.2% and 23.5%, respectively, while aggregates declined by 10.5% and asphalt by 8.6%.

The uneven market impact of the pandemic reflects sector-specific issues within construction, notably for those that are more exposed to general consumer and business confidence, such as for housing and commercial constructions.

Asphalt and aggregates sales were supported to a limited degree by continuity in road activity and some large infrastructure projects during the first lockdown, which was then followed by an acceleration during the second half of the year. As a result, on a quarterly basis, asphalt sales in 2020 Q4 exceeded pre-pandemic levels (up 5.8% compared with 2019 Q4). Similarly, aggregates sales were back to pre-pandemic levels.

However, the recovery in both ready-mixed concrete and mortar sales was slower, and volumes in 2020 Q4 remained lower compared with 2019 Q4. Demand in these sectors fell more significantly during the first lockdown, as housebuilding and commercial construction sites were mostly shut during the initial stages of the pandemic. Housebuilding saw a rapid subsequent recovery, fuelled by pent up demand and government initiatives like help to buy and lifting of stamp duty on some property. When work resumed it tended to involve the completion of existing sites rather than the start of new projects, providing only a limited boost to mortar sales.

The recovery in ready-mixed concrete sales was slowed by compounding weaknesses in commercial construction, including for retail, offices, hotels and other leisure facilities. Output in the commercial sector was already declining before the pandemic as a result of Brexit-related economic and political uncertainty, which reduced confidence and investment in the sector.

Widespread business closures due to the pandemic in the retail and hospitality sectors, alongside longer-term uncertainties on consumer habits and an accelerated move to online retail, as well as the potential for more working from home in the future, are weighing on the sector’s outlook.

Aurelie Delannoy, Director of Economic Affairs at the MPA, warns that, despite the encouraging rebound in demand for mineral products markets last year, the industry remains cautious.

“Sales volumes should continue to grow over 2021 and 2022, supported by the recovery of pandemic-related losses across all sub-sectors of construction and robust growth in new infrastructure work, including HS2. However, this outlook is beset with downside risks, not least due to the unknown future path of the pandemic and its potential wide-ranging impact on the UK economy and construction sector.

“As part of the government’s strategy to support the economy, the policy response so far has included an emphasis on infrastructure investment, including the announcement at the Spending Review 2020 of a new Levelling Up Fund for local infrastructure projects. This is is supported by the anticipated delivery of various five-year investment programmes in roads, rail and water & sewerage. However, infrastructure delivery is notoriously plagued by project delays and overrunning costs. Further unmet expectations in this area would not only be a clear setback for the recovery in construction and mineral products markets, but also significantly impact on business confidence and investment throughout the supply chain in an already challenging economic environment.”

Nigel Jackson, CEO at MPA, added: “While it is encouraging to see the sector recovering, there may be tough times ahead. The key thing is to get on with delivery of the planned infrastructure programme, turning lofty ambitions into concrete reality. We need to make the link between those ambitions and the supply chain for them, building on the government’s recognition of our sector’s essential status, which we have welcomed and is vital to help keep the economy moving.

“2020 was the most challenging year any of us can recall and recovering from it will take time. With cashflow challenges and project uncertainty, business needs continuing support and confidence-boosting measures to encourage investment.”

Mineral products sales volumes in Great Britain, change on the previous period (seasonally adjusted):